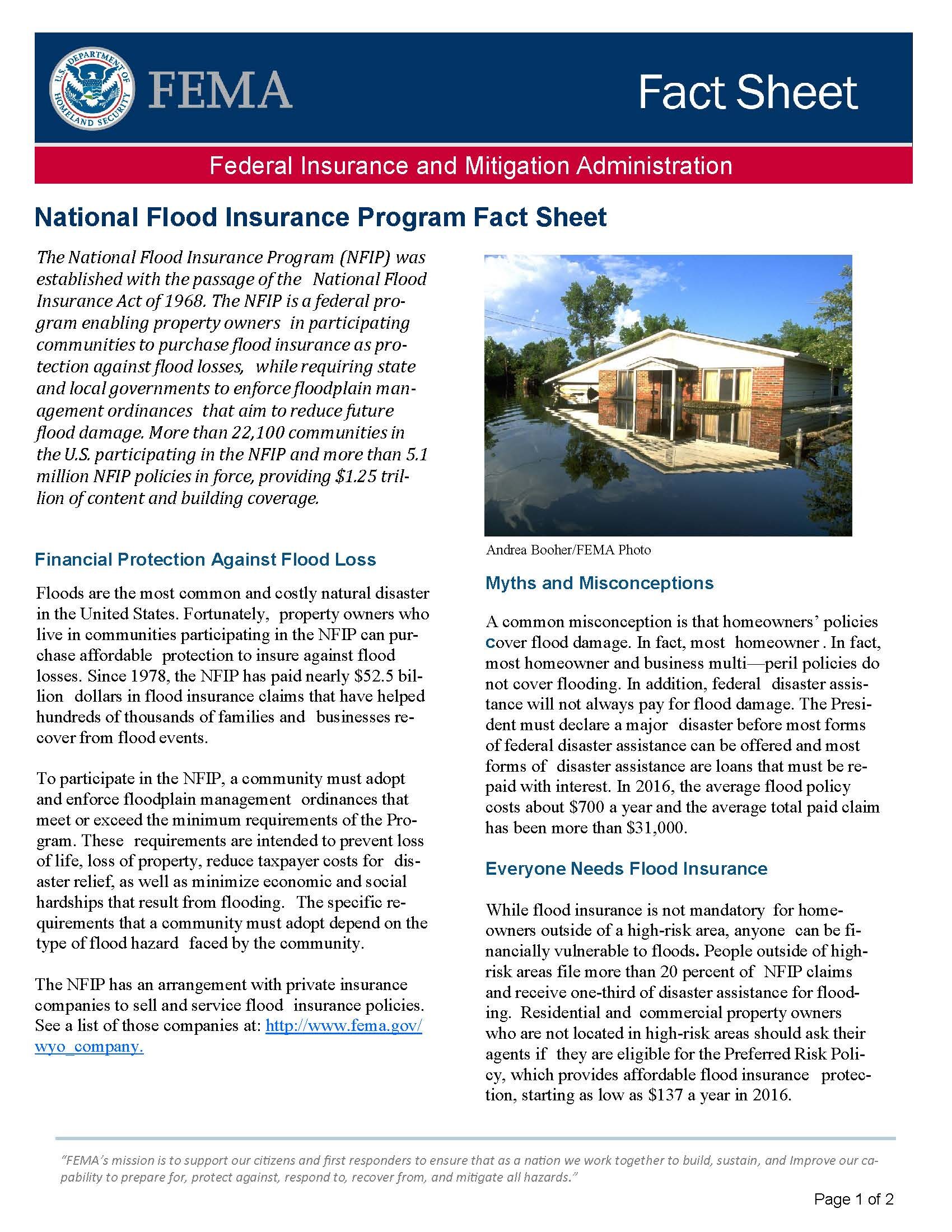

FLOOD INSURANCE

DID YOU KNOW?

When flooding is imminent or predicted, National Flood Insurance Program (NFIP) policyholders are eligible to receive up to $1,000 to purchase loss avoidance supplies like tarps, sandbags, and more.

GENERAL FLOOD INFORMATION

Call us at 800.332.6148 | 406.444.2040 for more information, or issues.

FLOOD FAQs

The terms of your policy will control what is covered or not covered in the case of flood damage.

Generally, flood damage caused by groundwater outside the home flowing into the home is not covered by your homeowner’s insurance policy. Flood damage caused by a broken pipe or other means that occurred inside the house may be covered.

If you have flood damage and are wondering if the damage is covered, review the terms of your policy, contact your agent, or contact the CSI.

You can obtain flood insurance through the National Flood Insurance Program (NFIP) if you live in a community that participates in this program. Click HERE to learn more or apply for NFIP flood insurance.

You can also obtain private flood insurance through your agent.

Private flood insurance policies may have shorter waiting periods. Check with your agent.

Federal disaster assistance is available only if the President declares a disaster. Such assistance typically comes in the form of a low-interest loan to help cover damage and must be repaid.

The cost of flood insurance varies by individual policy based on many factors.

Private flood insurance may be available in your area and be more affordable than insurance obtained through the National Flood Insurance Program. Check with your insurance agent for details about insurance available in your area.

Under federal law, the purchase of flood insurance is mandatory for all federal or federally-related financial assistance for the acquisition and/or construction of buildings in high-risk flood areas (Special Flood Hazard Areas or SFHAs). If the property is not in a high-risk area, but instead is in a moderate-to-low-risk area, federal law does not require flood insurance; however, a lender can still require it.

RESOURCES

- FEMA.gov or call FEMA Helpline at 800.621.3362

- FEMA Flood Insurance Fact Sheet

- FloodSmart Hotline—Experiencing Flooding? Call 888.379.9531